Neco Accounting questions and answers 2022

Here is the Neco Accounting questions and answers 2022

Neco Accounting answers 2022

NECO ACCOUNTING

F/Account+Obj!

1EACCECCAEA

11EBADCBBEBC

21BDCBCCBCDD

31ADCABCCDCA

41BAABBCEACA

51ABDABCEDBB

Completed

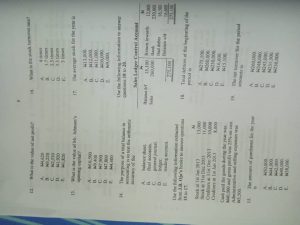

(1a)

DISCOUNT ALLOWED

– Discount allowed is granted by the seller to the buyer.

– The discount allowed is the expense of the seller.

– Discount allowed is debited in the books of the seller.

DISCOUNT RECEIVED

– The discount received is received by the buyer from the seller.

– Discount Received is an income of the buyer.

– Discount Received is credited in the books of the buyer.

(1b)

– Cash book

– Purchases book

– Sales book

– Purchases return or return outwards book

– Sales return or return inwards book

– Bills receivable book

(CHOOSE ANY 5)

(1c)

ERROR IT REVEALS

(i) Wrong Totaling of

(ii)Subsidiary Books

Posting of the Wrong Amount

ERROR THAT DOESN’T AFFECT IT

(i) Error of principle

(ii) Error of commission

(iii) Error of omission

NECO ACCOUNTING

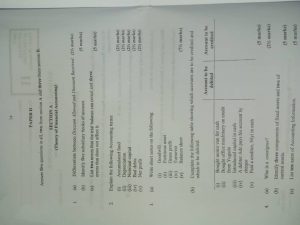

(2)

(i) Accumulated fund: An accumulated fund is a type of account that serves as the repository for funds that are collected over time by non-profit organizations and are above and beyond the money needed to cover operational and other expenditures.

(ii) Depreciation: It’s the reduction of a recorded cost of a fixed asset in a systematic manner until the value of the asset becomes zero or negligible.

(iii) Nominal Capital: It’s the amount of capital that a business can offer to shareholders, in the form of shares of stock. In most nations, the amount of this nominal share capital is regulated by governmental agencies that determine the financial stability of the business and the company’s ability to cover the value of those shares.

(iv) Bad debt: Bad debt is an expense that a business incurs once the repayment of credit previously extended to a customer is estimated to be uncollectible and is thus recorded as a charge off.

(v) Net profit: is the amount of money your business earns after deducting all operating, interest, and tax expenses over a given period of time.

NECO ACCOUNTING

(3a)

(i) Goodwill:

Goodwill is an intangible asset associated with the purchase of one company by another. Specifically, goodwill is recorded in a situation in which the purchase price is higher than the sum of the fair value of all visible solid assets and intangible assets purchased in the acquisition and the liabilities assumed in the process. The value of a company’s brand name, solid customer base, good customer relations, good employee relations, and any patents or proprietary technology represent some examples of goodwill.

(ii) Fictitious asset:

Fictitious assets have no physical existence or realisable value, but the company shows them as a cash expenditure in the books of accounts. They are a part of the assets column in the financial statements, and they are expenses or losses that do not get written off during the accounting period of their occurrence.

(iii) Gross profit:

Gross profit is the profit a company makes after deducting the costs associated with making and selling its products, or the costs associated with providing its services. Gross profit will appear on a company’s income statement and can be calculated by subtracting the cost of goods sold (COGS) from revenue (sales). These figures can be found on a company’s income statement. Gross profit may also be referred to as sales profit or gross income.

(iv) Turnover:

Turnover is an accounting concept that calculates how quickly a business conducts its operations. Most often, turnover is used to understand how quickly a company collects cash from accounts receivable or how fast the company sells its inventory.

(v) Balance sheet:

The term balance sheet refers to a financial statement that reports a company’s assets, liabilities, and shareholder equity at a specific point in time. Balance sheets provide the basis for computing rates of return for investors and evaluating a company’s capital structure. In short, the balance sheet is a financial statement that provides a snapshot of what a company owns and owes, as well as the amount invested by shareholders. Balance sheets can be used with other important financial statements to conduct fundamental analysis or calculate financial ratios.

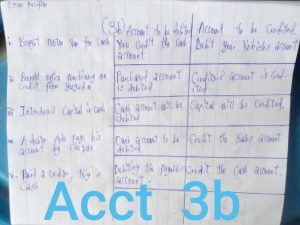

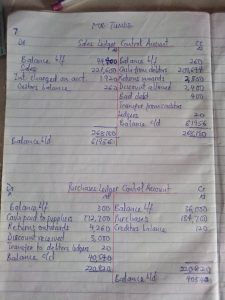

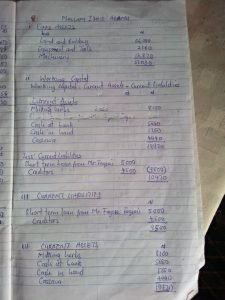

(3b) Loading.

What of number 9

Thanks but the images aren’t clear